Contents

Overview

A credit default swap (CDS) is a financial derivative contract where one party (the buyer) pays a premium to another party (the seller) in exchange for protection against a specific credit event, most commonly a default, on a particular debt instrument or borrower. Essentially, it functions like an insurance policy on debt. The buyer makes periodic payments, known as the 'spread,' to the seller. If the specified credit event occurs, the seller compensates the buyer, typically by paying the face value of the defaulted debt or the difference between the face value and the market value. Notably, CDS contracts can be purchased by parties who do not actually own the underlying debt, a practice known as 'naked' CDS, which amplifies their speculative and potentially destabilizing nature. The market for CDSs exploded in the early 2000s, reaching an estimated notional value of over $62 trillion by 2007, making them a critical, albeit often misunderstood, component of modern finance.

🎵 Origins & History

The concept of credit default swaps emerged from the need for sophisticated risk management tools in the burgeoning derivatives market. Initially conceived as a way for banks to offload credit risk from their balance sheets, the market was largely unregulated and opaque. By the late 1990s and early 2000s, the market began to expand dramatically, fueled by the growth of securitization and the increasing complexity of financial instruments. The development of standardized contracts by organizations like the International Swaps and Derivatives Association (ISDA) facilitated this growth, making CDSs more accessible and liquid. This period saw the rise of entities like AIG as major sellers of credit protection, a role that would later prove catastrophic.

⚙️ How It Works

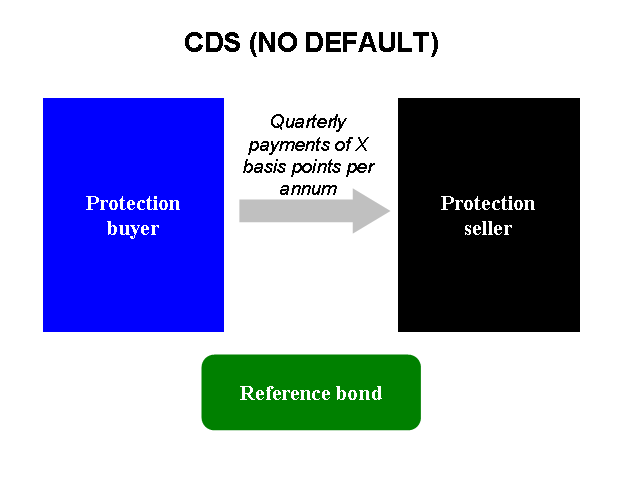

At its core, a CDS is a bilateral contract between two parties: a protection buyer and a protection seller. The buyer pays a regular fee, the 'spread,' to the seller, much like an insurance premium. In return, the seller agrees to make a payment to the buyer if a predefined 'credit event' occurs with respect to a specific 'reference entity' (e.g., a company or sovereign nation) and its 'reference obligation' (e.g., a particular bond). Common credit events include bankruptcy, failure to pay, and restructuring. Upon the occurrence of a credit event, the buyer typically has two settlement options: physical settlement, where the buyer delivers the defaulted debt to the seller and receives its face value, or cash settlement, where the seller pays the buyer the difference between the face value and the market value of the defaulted debt. The pricing of CDSs, or their spreads, reflects the perceived creditworthiness of the reference entity; higher spreads indicate higher perceived risk.

📊 Key Facts & Numbers

The notional value of the global CDS market reached an astonishing peak, according to the Bank for International Settlements (BIS). The average spread for a 5-year CDS on a corporate entity can range from as low as 50 basis points (0.5%) for highly-rated companies to over 1000 basis points (10%) for distressed borrowers. For sovereign debt, spreads can fluctuate wildly; for instance, Greek sovereign CDS spreads surged to over 5000 basis points (50%) during the European sovereign debt crisis in 2012. The total value of CDS contracts outstanding is often significantly larger than the actual amount of debt in existence, a phenomenon that contributed to the 2008 financial crisis.

👥 Key People & Organizations

While no single individual can be solely credited with the invention of CDSs, key organizations that shaped the CDS market include the ISDA, which standardized contracts and protocols, and major financial institutions that acted as both buyers and sellers of protection, such as Goldman Sachs, Morgan Stanley, Citigroup, and notably, AIG, whose massive exposure to CDSs nearly led to its collapse in 2008. Regulatory bodies like the U.S. Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) have since increased oversight.

🌍 Cultural Impact & Influence

Credit default swaps have profoundly influenced the global financial landscape, acting as both a tool for risk management and a catalyst for systemic instability. Their proliferation in the early 2000s, particularly in relation to collateralized debt obligations (CDOs) and subprime mortgages, played a central role in the 2008 financial crisis. The ability to trade 'naked' CDSs allowed for massive speculative bets on the failure of companies and even nations, creating a complex web of interconnectedness. The movie 'The Big Short' brought the mechanics and implications of CDSs to a wider audience, illustrating how some investors profited from the impending collapse of the housing market by buying CDS protection. The cultural impact is one of increased skepticism towards complex financial instruments and a demand for greater transparency.

⚡ Current State & Latest Developments

In the post-2008 era, the CDS market has undergone significant regulatory reform, aiming to increase transparency and reduce systemic risk. The Dodd-Frank Act in the United States mandated that many CDS contracts be cleared through central clearinghouses, rather than being traded solely over-the-counter (OTC). This aims to reduce counterparty risk, as the clearinghouse guarantees the trade. Despite these reforms, the market remains substantial, though its notional value has decreased from its 2007 peak. Recent developments include increased trading in sovereign CDSs, particularly in emerging markets, and ongoing debates about the appropriate level of capital requirements for CDS sellers. The market continues to be a bellwether for credit market sentiment, with spreads widening during periods of economic uncertainty, such as the COVID-19 pandemic in early 2020.

🤔 Controversies & Debates

The most significant controversy surrounding credit default swaps centers on their role in the 2008 global financial crisis. Critics argue that the ability to buy 'naked' CDSs, without owning the underlying debt, allowed for excessive speculation and created incentives for parties to bet on the failure of entities they had no direct exposure to. This practice, exemplified by the massive bets against AIG and Lehman Brothers, amplified losses and contributed to a 'too big to fail' mentality. Another point of contention is the opacity of the OTC market, which made it difficult for regulators and market participants to assess the true extent of risk exposure. The debate continues over whether CDSs are primarily tools for hedging risk or instruments for pure speculation, and whether the regulatory changes implemented since 2008 have been sufficient to prevent another systemic meltdown.

🔮 Future Outlook & Predictions

The future of credit default swaps will likely be shaped by ongoing regulatory evolution and the persistent demand for sophisticated credit risk management tools. Central clearing is expected to become more widespread, potentially reducing counterparty risk but also concentrating it within clearinghouses, which themselves require robust capital and oversight. The market may see further innovation in contract design, potentially leading to more tailored hedging solutions or new forms of speculative instruments. As global debt levels continue to rise, particularly sovereign debt in developed and emerging economies, the demand for CDSs as a hedging mechanism is likely to persist. However, the specter of the 2008 crisis will continue to cast a long shadow, ensuring that regulatory scrutiny and public debate surrounding these instruments remain intense. The potential for a significant credit event in a major economy could reignite calls for even stricter controls.

💡 Practical Applications

Credit default swaps serve a crucial function in modern finance by allowing investors and institutions to manage and transfer credit risk. For instance, a bank that has issued a large loan to a corporation might buy a CDS to protect itself against the possibility of that corporation defaulting on its debt. This allows the bank to free up capital or reduce its risk profile. Similarly, an investor holding a portfolio of bonds might purchase CDSs to hedge against potential defaults within that portfolio, thereby stabilizing returns.

Key Facts

- Category

- finance

- Type

- topic