Contents

Overview

The roots of financial reporting stretch back to ancient Mesopotamia, where clay tablets recorded agricultural yields and trade transactions, laying the groundwork for systematic record-keeping. Double-entry bookkeeping, credited to Luca Bartolomeo Pacioli in his 1494 treatise "Summa de Arithmetica, Geometria, Proportioni et Proportionalita," revolutionized accounting by introducing the concept of debits and credits, making it possible to track financial flows with unprecedented accuracy. The Industrial Revolution in the 18th and 19th centuries amplified the need for formal financial reporting as joint-stock companies grew in scale and complexity, requiring investors to assess risk and return. Early stock exchanges in London and New York demanded standardized disclosures, leading to the formation of professional accounting bodies and the gradual development of accounting principles that would eventually coalesce into modern frameworks like Generally Accepted Accounting Principles in the United States and International Financial Reporting Standards globally.

⚙️ How It Works

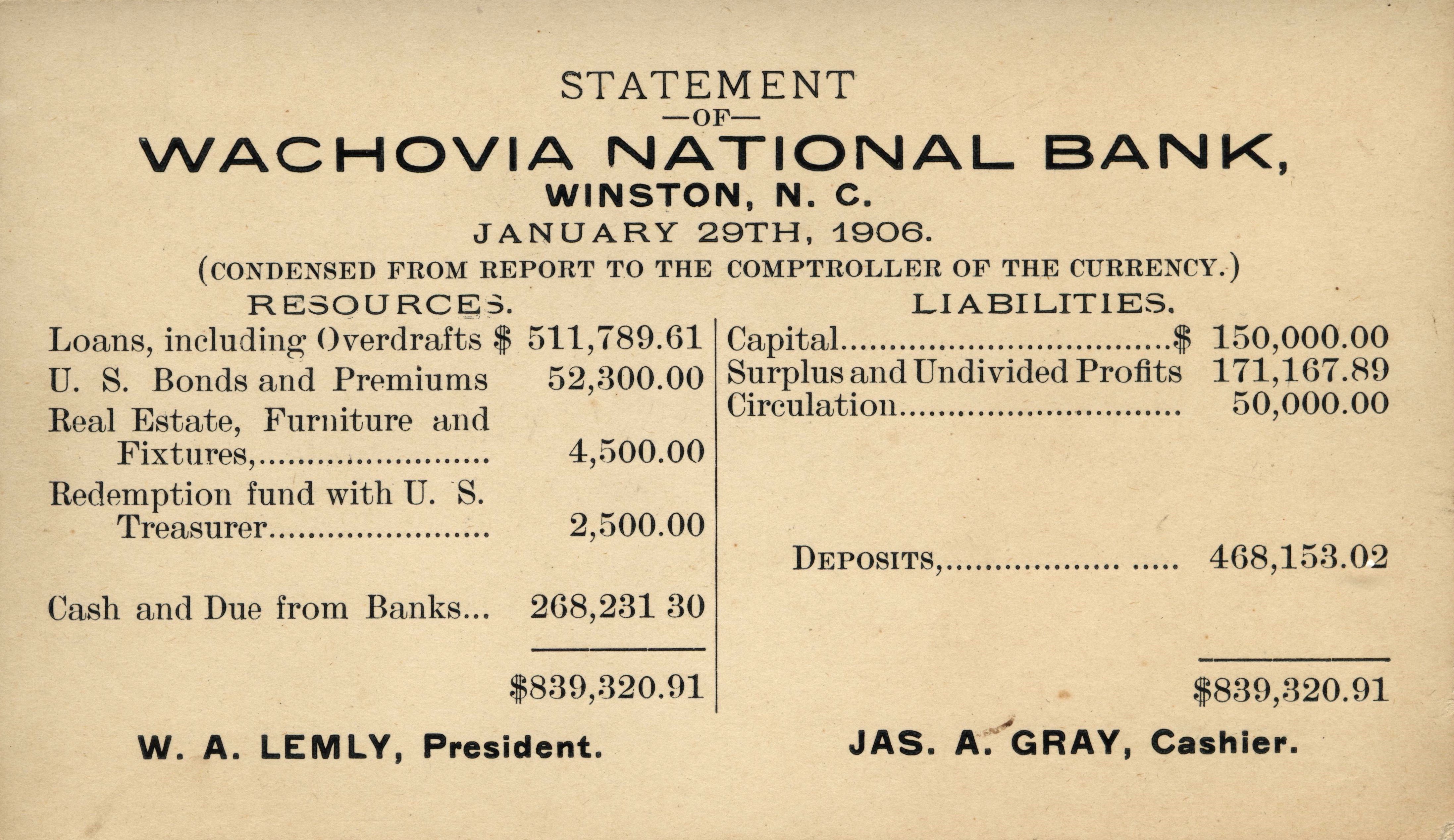

At its core, financial reporting involves collecting transactional data, classifying it into categories like assets, liabilities, revenues, and expenses, and then summarizing this information into standardized financial statements. The balance sheet provides a snapshot of an entity's financial health at a specific point in time, detailing what it owns (assets), what it owes (liabilities), and the owners' stake (equity). The income statement (or profit and loss statement) reveals financial performance over a period, showing revenues earned and expenses incurred to arrive at net income or loss. The cash flow statement tracks the movement of cash in and out of the business from operating, investing, and financing activities, crucial for assessing liquidity. These statements are typically accompanied by notes that provide further detail and context, ensuring transparency and comprehensibility for users like investors, creditors, and regulators.

📊 Key Facts & Numbers

Globally, financial reporting is increasingly influenced by digital transformation. The accounting software market, which underpins much of financial reporting, is projected to reach $10.5 billion by 2027, highlighting the immense scale of the industry. Furthermore, the average cost for a public company to prepare and audit its annual financial statements can range from $1 million to $5 million, underscoring the significant investment in this process.

👥 Key People & Organizations

Key figures in the development of financial reporting include Luca Pacioli, whose 1494 work codified double-entry bookkeeping, and George O. May, a pivotal figure in shaping Generally Accepted Accounting Principles in the early 20th century. Organizations like the Financial Accounting Standards Board (FASB) in the US and the International Accounting Standards Board (IASB) are instrumental in setting and evolving accounting standards. Regulatory bodies such as the Securities and Exchange Commission in the United States and the European Securities and Markets Authority (ESMA) oversee compliance and enforce reporting requirements. Prominent accounting firms like Deloitte Touche Tohmatsu Limited, PricewaterhouseCoopers, Ernst & Young, and KPMG International play a critical role in auditing financial statements and providing assurance.

🌍 Cultural Impact & Influence

Financial reporting is the lingua franca of the global business world, profoundly influencing investment decisions, capital allocation, and economic growth. The transparency it provides allows investors to assess risk and return, fueling markets and enabling companies to raise capital for expansion. Conversely, opaque or misleading reporting can lead to catastrophic financial crises. The widespread adoption of standardized reporting frameworks like International Financial Reporting Standards has fostered greater comparability across international markets, facilitating cross-border investment and economic integration.

⚡ Current State & Latest Developments

The current landscape of financial reporting is increasingly dominated by digital transformation and the integration of artificial intelligence and machine learning. Companies are moving towards real-time reporting capabilities, enabled by cloud-based accounting systems and eXtensible Business Reporting Language (XBRL) for structured data tagging. The push for greater environmental, social, and governance (ESG) disclosures is also a major development, with organizations like the International Sustainability Standards Board (ISSB) working to standardize sustainability reporting. The ongoing debate about the optimal balance between detailed disclosure and information overload continues, with regulators and standard-setters grappling with how to ensure reports are both comprehensive and digestible for a diverse range of stakeholders.

🤔 Controversies & Debates

One of the most persistent controversies in financial reporting revolves around the inherent tension between providing sufficient detail and avoiding information overload. Critics argue that the sheer volume of disclosures, particularly in the notes to financial statements, can obscure critical information. Another significant debate concerns the use of estimates and judgments in accounting, which can allow for manipulation, as evidenced by numerous accounting scandals. The comparability of financial statements across different jurisdictions, despite efforts like International Financial Reporting Standards, remains a challenge due to differing interpretations and enforcement. Furthermore, the role and independence of auditors are frequently scrutinized, especially when major accounting failures occur, raising questions about the effectiveness of the assurance process.

🔮 Future Outlook & Predictions

The future of financial reporting points towards greater automation, real-time data analytics, and integrated reporting that combines financial, operational, and ESG metrics. AI is expected to automate many routine reporting tasks, freeing up finance professionals for more strategic analysis. The demand for integrated reporting, which presents a more holistic view of an organization's performance and value creation, is likely to grow, potentially leading to new reporting frameworks. There's also a growing expectation for more forward-looking information, moving beyond historical performance to predictive insights, though this presents significant challenges in terms of reliability and standardization. The increasing focus on Environmental, Social, and Governance factors will undoubtedly lead to more robust and standardized sustainability disclosures.

💡 Practical Applications

Financial reporting is indispensable for a multitude of practical applications. For investors, it's the primary tool for evaluating potential investments, assessing risk, and making buy/sell decisions. Lenders rely on financial statements to determine creditworthiness and the ability of a borrower to repay loans. Management uses these reports for internal decision-making, performance evaluation, strategic planning, and resource allocation. Regulators, such as tax authorities and securities commissions, use financial reports to ensure compliance with laws and regulations, detect fraud, and maintain market integrity. Even employees can use financial reports to gauge the health and stability of their employer, influencing their career decisions.

Key Facts

- Category

- technology

- Type

- topic