Contents

Overview

The seeds of the 2000s United States housing bubble were sown in the early years of the new millennium, fueled by a Federal Reserve policy of keeping interest rates exceptionally low following the dot-com bust and the September 11th attacks. This accommodative monetary policy, coupled with a belief in ever-rising home values, encouraged a surge in mortgage originations, particularly subprime and Alt-A loans, which were often issued with minimal documentation or to borrowers with questionable creditworthiness. Financial innovation, such as the widespread securitization of mortgages into CDOs and MBS, allowed lenders to offload risk and created a seemingly insatiable demand for new mortgages, irrespective of borrower quality. This created a feedback loop where rising prices encouraged more borrowing and investment, further inflating the bubble. Key precursors include the Savings and Loan crisis of the 1980s, which demonstrated the dangers of unchecked real estate speculation and lax regulation, though the scale and complexity of the 2000s bubble far surpassed previous episodes.

⚙️ How It Works

The mechanics of the housing bubble involved a cascading series of financial instruments and market behaviors. Lenders, incentivized by origination fees and the ability to sell loans into the secondary market, relaxed underwriting standards, offering adjustable-rate mortgages (ARMs) with low initial 'teaser' rates and 'liar loans' that required little proof of income. These mortgages were then bundled by investment banks like Lehman Brothers and Bear Stearns into complex financial products, such as CDOs, which were sliced into tranches with varying levels of risk and return. Credit rating agencies, such as S&P and Moody's, often assigned high ratings to these securities, masking their underlying risk. When interest rates began to rise and housing prices plateaued and then declined, borrowers with ARMs faced sharply higher payments, leading to defaults and foreclosures. This influx of distressed properties onto the market further depressed prices, triggering a downward spiral.

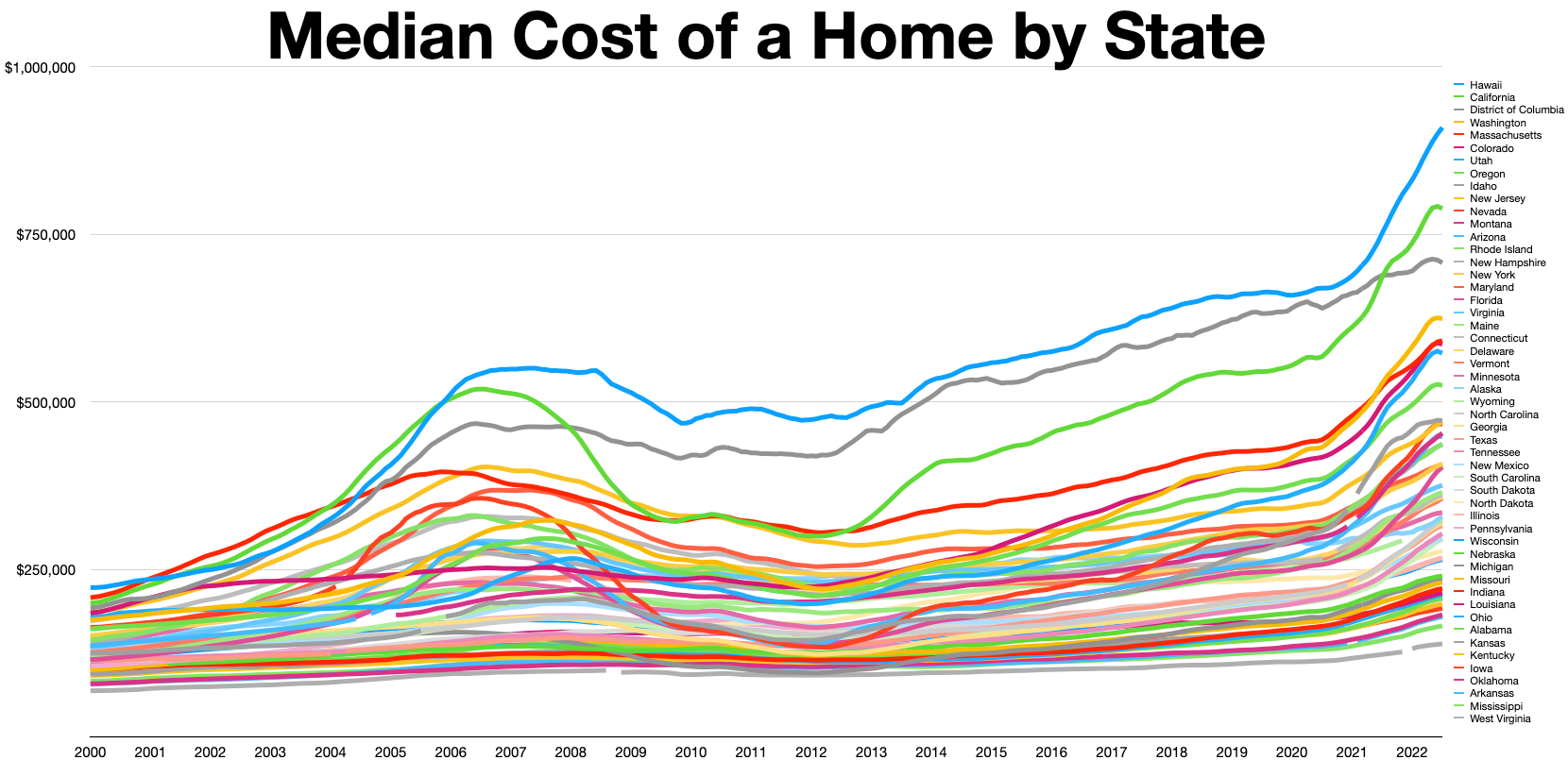

📊 Key Facts & Numbers

Numerous individuals and institutions played pivotal roles in the housing bubble and its aftermath. Federal Reserve Chairman Alan Greenspan is often criticized for maintaining low interest rates for too long, which is seen as a significant catalyst for the bubble. Key figures in the financial industry, such as Lehman Brothers CEO Richard Fuld Jr. and Bear Stearns CEO James Cayne, presided over firms that collapsed under the weight of their subprime mortgage exposure. Henry Paulson, as U.S. Secretary of the Treasury during the crisis, orchestrated government bailouts and interventions, including the controversial rescue of AIG. The role of mortgage lenders like Countrywide Financial and New Century Financial in originating risky loans is also central to the narrative. Regulatory bodies like the SEC and the Federal Reserve faced scrutiny for their oversight failures.

👥 Key People & Organizations

The cultural resonance of the housing bubble is profound, permeating popular culture and shaping public discourse on finance and inequality. Films like 'The Big Short' (2015) and 'Inside Job' (2010) reportedly brought the complexities of the crisis to a mainstream audience, highlighting the perceived greed and malfeasance of Wall Street. The term 'foreclosure' became a familiar part of the American lexicon during the housing crisis, symbolizing financial ruin for millions. The crisis also fueled widespread distrust in financial institutions and government regulators, contributing to populist movements and a heightened awareness of economic disparities. The dream of homeownership was tarnished for many due to the housing bubble, leading to a reevaluation of housing as a stable investment versus a fundamental need.

🌍 Cultural Impact & Influence

While the most acute phase of the housing bubble collapse reportedly occurred between 2007 and 2011, its effects continue to ripple through the U.S. economy. In the years following the Great Recession, housing markets in many areas experienced slow recoveries, with some regions still struggling to reach pre-bubble price levels. Regulatory reforms, such as the Dodd-Frank Act, were implemented to prevent a recurrence, introducing stricter capital requirements for banks and establishing the Consumer Financial Protection Bureau (CFPB) to oversee mortgage lending. However, debates persist about the effectiveness of these reforms and whether new vulnerabilities have emerged, particularly in areas like non-bank mortgage servicing and the rise of institutional investors in the single-family rental market. The lingering impact on generational wealth and homeownership rates remains a significant concern.

⚡ Current State & Latest Developments

The housing bubble's origins and collapse are subjects of intense debate. A central controversy revolves around the degree to which the Federal Reserve's monetary policy was responsible versus the predatory practices of lenders and the failures of financial innovation. Skeptics of the 'easy money' narrative point to the widespread issuance of subprime mortgages even before the Fed's most aggressive rate cuts, suggesting systemic issues within the lending industry itself. The role of government-sponsored enterprises like Fannie Mae and Freddie Mac in purchasing and guaranteeing mortgages is another contentious point. Furthermore, the effectiveness and fairness of the government's response, including the Troubled Asset Relief Program (TARP), remain hotly debated, with critics arguing that bailouts favored financial institutions over homeowners.

🤔 Controversies & Debates

Looking ahead, the specter of housing bubbles remains a concern for economists and policymakers. While current lending standards are generally tighter than in the pre-2008 era, factors such as sustained low interest rates, increased foreign investment in U.S. real estate, and the growing influence of institutional investors in the housing market could create new inflationary pressures. Predictive models vary widely, with some forecasting continued moderate price appreciation and others warning of potential regional overheating. The long-term impact of remote work on housing demand and affordability in different geographic areas is another significant unknown. Policymakers face the ongoing challenge of balancing housing affordability with financial stability, a delicate act that proved disastrously difficult in the early 2000s.

🔮 Future Outlook & Predictions

The primary practical application of understanding the housing bubble lies in risk management and policy formulation. For financial institutions, lessons learned inform underwriting standards, risk assessment for mortgage-backed securities, and capital adequacy requirements. Regulators use the bubble's history to design and enforce consumer protection laws, monitor systemic risk, and implement monetary policy with a keener eye on asset price inflation. For individual investors and homeowners, knowledge of past bubbles serves as a cautionary tale against speculative excess and over-leveraging. Understanding the indicators of a potential bubble—rapid price appreciation, high loan-to-value ratios, and increased speculative activity—can help individuals make more informed decisions about buying, selling, or investing in real estate.

Key Facts

- Category

- history

- Type

- topic