Contents

Overview

The roots of the 2000s housing bubble can be traced to the early years of the decade, following the dot-com bust and the September 11th attacks. The Federal Reserve, under Chairman Alan Greenspan, aggressively lowered interest rates to stimulate the economy. This cheap credit environment made mortgages exceptionally affordable, igniting demand for housing. Simultaneously, a shift in lending practices saw the rise of subprime mortgages, extended to borrowers with poor credit histories, and exotic loan products like adjustable-rate mortgages (ARMs) and interest-only loans. Financial institutions, eager for returns, packaged these mortgages into mortgage-backed securities (MBS) and CDOs, which were then sold to investors worldwide, often with inflated credit ratings from agencies like Moody's and S&P. This created a seemingly insatiable demand for more mortgages, further incentivizing lenders to loosen standards and push more loans, regardless of borrower quality.

⚙️ How It Worked: The Mechanics of the Boom

The housing bubble operated on a feedback loop of rising prices and easy credit. As home values climbed, homeowners could easily refinance or take out home equity loans, using their increased equity to spend more, which in turn further boosted demand and prices. Lenders, protected by the securitization process and often assured by credit rating agencies, felt less risk in issuing loans to less-qualified borrowers. The proliferation of "no-doc" or "liar's loan", which required minimal income verification, exemplified the extreme relaxation of underwriting standards. Complex financial instruments like credit default swaps (CDS) were also developed, ostensibly to insure against default but ultimately creating a speculative market that amplified risk. When interest rates began to rise in 2004-2006, and borrowers with ARMs faced payment shock, the unsustainable nature of the boom became apparent.

📊 Key Facts & Numbers

The scale of the housing bubble was staggering. By the end of 2007, over 2.3 million households were in some stage of foreclosure, a number that surged to over 3.9 million in 2008. The financial sector bore the brunt, with major institutions like Lehman Brothers collapsing in September 2008, and others like AIG requiring massive government bailouts. The U.S. Gross Domestic Product (GDP) contracted by 4.3% in 2009, the largest annual decline since 1946, directly linked to the crisis.

👥 Key People & Organizations

Several key figures and organizations were central to the housing bubble and its aftermath. Alan Greenspan, as Federal Reserve Chairman from 1987 to 2006, presided over the period of low interest rates that fueled the boom. Ben Bernanke, his successor, faced the full brunt of the crisis and implemented unconventional monetary policies. Henry Paulson, U.S. Treasury Secretary during the crisis, spearheaded the Troubled Asset Relief Program (TARP) to stabilize financial markets. Major financial institutions like Bank of America, Citigroup, and JPMorgan Chase were deeply involved in mortgage origination and securitization. The rating agencies, Moody's, S&P, and Fitch Ratings, played a critical role by assigning high ratings to risky MBS and CDOs. The Federal Reserve and the Securities and Exchange Commission (SEC) were criticized for their regulatory oversight failures.

🌍 Cultural Impact & Influence

The cultural impact of the housing bubble was profound, embedding the idea of homeownership as a guaranteed path to wealth into the American psyche. The dream of the "American Dream" became inextricably linked to rising property values, leading many to overextend themselves financially. The subsequent crash shattered this illusion for millions, leading to widespread loss of savings, displacement through foreclosures, and a deep erosion of trust in financial institutions and government regulators. The crisis also fueled a surge in investigative journalism and public discourse about economic inequality, predatory lending, and the ethics of Wall Street. The visual of vacant homes and "for sale" signs became a stark symbol of the era's economic devastation, influencing art, literature, and film for years to come.

⚡ Current State & Latest Developments

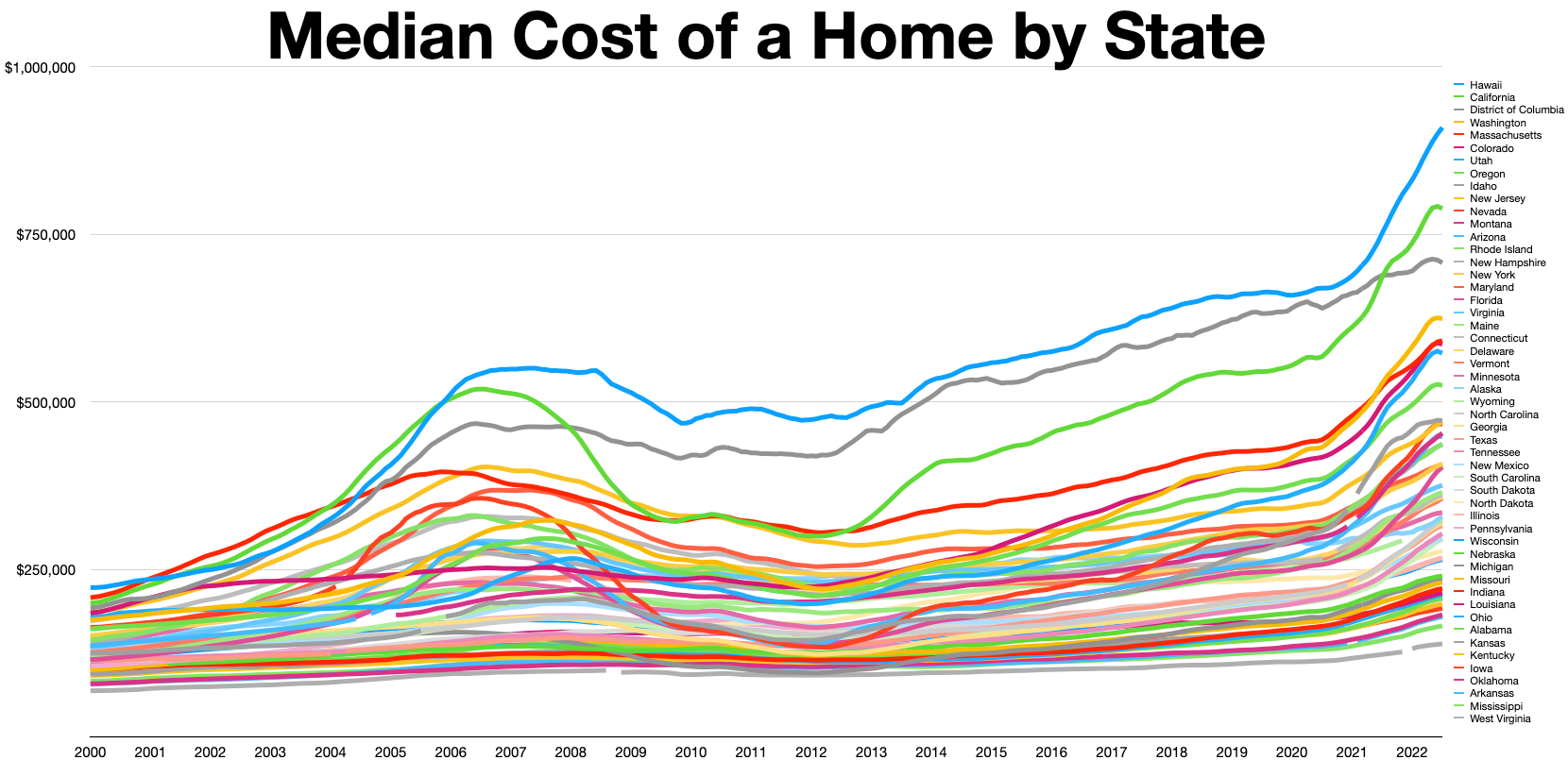

In the years following the 2008 crisis, significant regulatory reforms were enacted, most notably the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010. This legislation aimed to increase transparency, regulate derivatives, and establish the Consumer Financial Protection Bureau (CFPB) to protect consumers from predatory financial practices. While housing prices have largely recovered and even surpassed pre-crisis peaks in many markets, the lessons learned continue to shape lending standards and financial regulation. The debate over whether a new bubble is forming, particularly in certain high-demand urban areas, remains a recurring theme in economic discussions, highlighting the lingering sensitivity to housing market dynamics.

🤔 Controversies & Debates

The housing bubble is a subject of intense controversy and debate. A central point of contention is the extent to which the Federal Reserve's monetary policy, particularly the low interest rates of the early 2000s, was responsible for inflating the bubble, versus the role of deregulation and predatory lending practices. Critics argue that Greenspan and the Fed should have recognized and acted upon the warning signs sooner. Another major debate surrounds the culpability of financial institutions and rating agencies; while many executives faced no criminal charges, the ethical implications of securitizing and selling toxic assets remain a sore point. The effectiveness and fairness of the government bailouts, particularly TARP, are also heavily debated, with some arguing they were necessary to prevent total collapse while others decry them as rewarding reckless behavior.

🔮 Future Outlook & Predictions

The future outlook regarding housing bubbles remains a subject of ongoing analysis. Economists and policymakers are keenly aware of the potential for similar speculative cycles, though the regulatory environment is now more robust. The increasing role of institutional investors in the single-family rental market, the impact of rising construction costs, and the persistent housing affordability crisis in many major cities are all factors that could influence future market dynamics. Some analysts predict a continued, albeit slower, appreciation in housing values driven by demographic trends and limited supply, while others warn of potential overvaluation in certain overheated markets, particularly those influenced by speculative investment and foreign capital. The long-term impact of remote work on housing demand in suburban and rural areas also presents an unpredictable variable.

💡 Practical Applications

The primary practical application of understanding the 2000s housing bubble lies in risk management and regulatory policy. For financial institutions, the crisis underscored the importance of rigorous underwriting, diversification of assets, and transparent risk assessment. For regulators, it highlighted the need for robust oversight of financial markets, particularly complex derivatives and securitization processes, and the critical role of consumer protection. For individual homeowners and investors, the bubble serves as a stark reminder of the volatility inherent in real estate markets and the dangers of assuming continuous price appreciation. It informs personal financial planning, emphasizing the need for realistic expectations and avoiding excessive leverage, particularly when purchasing a primary residence.

Key Facts

- Category

- history

- Type

- topic